Traditional vs Parametric Insurance Billing: Core Differences

The fundamental divide between understanding traditional and parametric insurance comes down to a single question: Are you being paid for what you lost, or for an event that happened? The difference appears small, but it transforms nearly everything about how a policy is billed, priced, and paid out.

For corporate risk officers, commercial insurance brokers, CFOs, and risk managers, navigating this evolving landscape is no longer optional. This comprehensive guide breaks down the structural, financial, and operational differences between traditional and parametric insurance billing, giving you the clarity needed to optimize your corporate risk portfolio.

Traditional vs Parametric Insurance Billing: The Core Difference

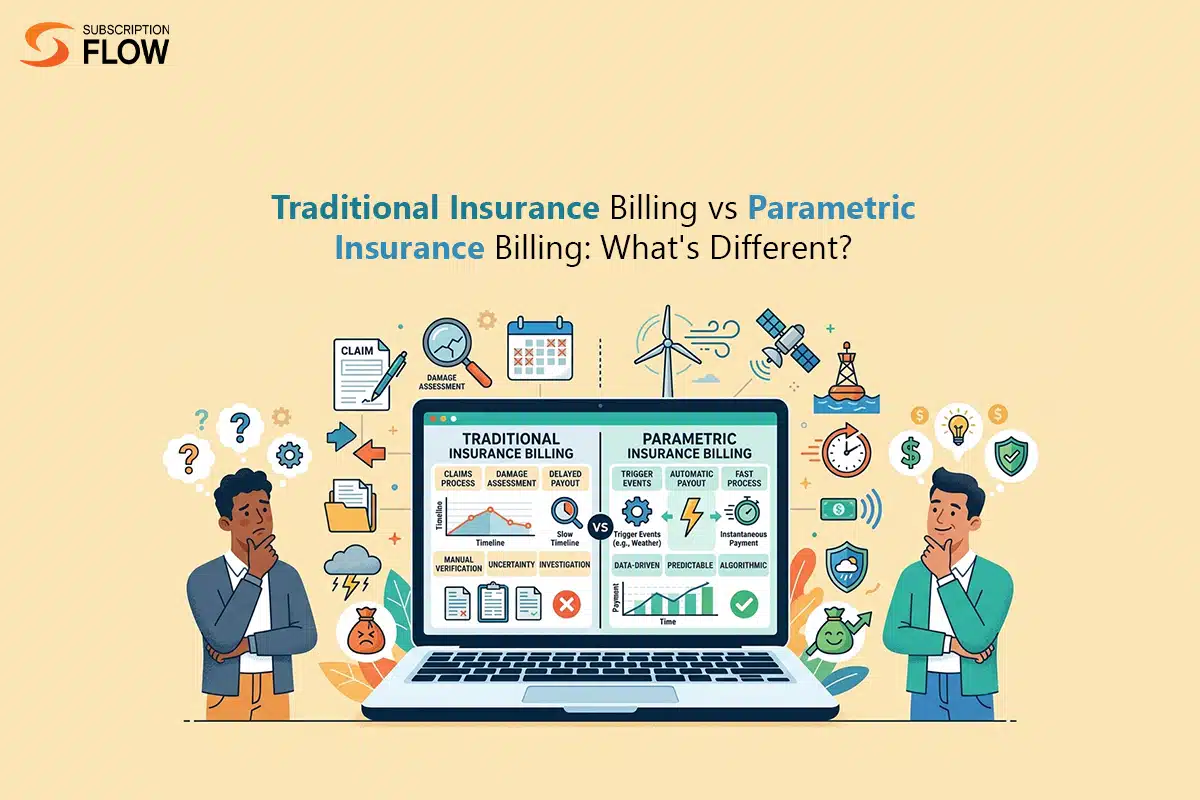

In simple words, traditional insurance billing is loss-based, while parametric insurance billing is trigger-based. Loss-based means that whenever something goes wrong, the insurer physically assesses the actual damage and then adjusts the compensation accordingly.

On the other hand, trigger-based refers to a pre-decided payout when a trigger is hit. This means you pay a premium tied to the probability and severity of a defined event. For instance, a trigger is set for an earthquake above a certain magnitude or rainfall below a set threshold, and the insurer pays a pre-agreed amount automatically, with no damage assessment.

The traditional billing is useful when your priority is accuracy of payout relative to loss, while opting for parametric billing when speed and certainty of payout relative to a measurable event are required.

How Traditional Insurance Billing Works

The principle of indemnity lies at the foundation of traditional commercial insurance. The aim of traditional insurance billing is to offer a payout that matches the exact loss of the policyholder. Considering the high accuracy, premium billing and claims, payout processes are highly customised, require detailed manual input, and are inherently retroactive.

It operates in two phases: the premium side, which occurs before an actual loss happens, and the claim side that starts after the incident occurs.

The Premium Billing Side

This includes a detailed underwriting process in which insurers collect regular payments (premiums) against the policies owed to maintain the active coverage. Insurers estimate asset values, claims history, location-specific risk factors, industry classification, and coverage limits. Since the risk profile change, traditional billing usually includes:

- Upfront deposits and audits: Most of the policies require an estimated upfront payment, followed by an end-of-year audit where your actual payroll or revenue is checked, wrestling in a supplemental bill or a return premium.

- Layered programs: Large corporate programs need billing across several tranches of insurers (primary layers, excess layers), complicating accounts payable.

For the final billed amount, endorsements, deductibles, and policy limits are taken into consideration depending on variable exposures such as payroll or revenue.

The Claim and Payout Side

Billing logic shifts entirely on the claim side. Whenever the incident occurs, the policy owner files a claim, and an insurer is assigned to investigate the actual loss. Damages, documentation, pictorial evidence, etc., are collected by the adjuster who determines the final payout. It is a multi-step process that includes:

- First notice of loss (FNOL): A comprehensive claim report is filed by the policyholder

- Investigation and Adjusting: The insurer appoints a loss adjuster who physically examines properties, reviews financial ledgers, and examines all circumstances.

- Proof of loss: Compilation of extensive documentation, such as receipts, contractor estimates, business interruption financial logs, etc, is done to give proof of claim against the damage.

- Deductible application: Loss is verified and calculated, and the policyholder’s deductible is subtracted from the final billing settlement.

This is highly useful in protecting against overpayment and fraud, but also takes weeks and months to resolve, especially for complicated or disputed losses.

How Parametric Insurance Billing Works

Instead of paying for what is lost, parametric insurance billing pays for what happened, as measured against an objective, pre-agreed index. It is more transparent and uses advanced stochastic modelling (simulating thousands of data scenarios) to price the policy.

- The trigger and the index: The meter being tracked is called the index, while the specific threshold of that metric is known as the trigger. Both index and trigger are kept objective, measurable in real-time, and maintained by a third party referred to as oracle.

- The pre-agreed payout: Parametric policies pre-decide the payout structures at the time policies are written. They either account for a single lump sum triggered at one threshold or a tiered structure where the payout scales with the severity of the event.

- Disbursement: Payout is disbursed the moment a third-party source confirms that the trigger threshold has been breached. There’s no need for proof of loss. The amount is wired into the policyholder’s bank account within 3 to 14 days of the event.

Parametric premiums can be quoted quickly since they don’t require the same depth of asset-specific underwriting, which is part of why these policies are often used to supplement, rather than replace, traditional coverage.

Key Differences At a Glance

To understand how these two frameworks differ, review the following comparison table.

| Feature | Traditional Insurance Billing | Parametric Insurance Billing |

| Payout basis | Actual assessed loss (indemnity) | Pre-agreed amount tied to a measured trigger |

| Speed of payout | Weeks to months | Days, sometimes near-instant |

| Adjuster needed | Yes | No |

| Proof of loss | Complete proof (receipts, inspections, estimates) | Not required, only data verification |

| Premium pricing basis | Asset values, claims history, individual risk profile | Historical frequency / severity of index event |

| Dispute potential | Higher (over damage valuation and scope) | Lower (limited to whether the trigger was met) |

| Best use cases | Property damage, liability, complex or variable losses | Natural catastrophe gaps, business interruption, agriculture, fast liquidity needs |

Pros and Cons of Traditional Insurance Billing

Pros:

- Accurate estimation of loss

- Comprehensive coverage

Cons:

- Delayed payouts

- Complex billing process

- Administrative burden

Pros and Cons of Parametric Insurance Billing

Pros:

- Instant payouts

- No need for excessive proofs and documentation

- Flexible use of funds

- Unique accessible coverage

Cons:

- Inaccurate estimation of specific loss

- Risk of underpayment/overpayment

- Data dependency

Why the Billing Model Matters in Practice

The billing model decides the outcome of a policy. Therefore, the structural mechanics of how money flows in and out of your insurance program have massive real-world implications for a company’s financial health, operational resilience, and balance sheet stability.

Cash Flow and Speed

Cash acts as oxygen when a crisis occurs. Traditional insurance billing usually leaves a company suffocating while waiting for funds. Parametric payouts, arriving in days, are designed specifically to close that gap, providing liquidity exactly when it’s needed most, even if the amount doesn’t perfectly match the actual loss.

Transparency

Parametric policies offer improved transparency. Both parties know, in advance, exactly what triggers a payout and exactly how much that payout is. There’s little room for subjective disagreement once the data comes in. Traditional policies offer transparency of a different sort: the payout is tied directly to demonstrated loss, which can feel fairer in cases where the actual damage is far different than what a generic trigger would have predicted.

Administrative Cost

Traditional claims handling is labor-intensive: adjusters, investigators, documentation review, and sometimes legal involvement all add cost and time. Parametric claims processing is comparatively lean, since the entire payout decision rests on verifying data against a threshold. That efficiency is part of why parametric products can be priced competitively for certain risks, even though it comes with trade-offs in precision.

Predictability

With parametric insurance billing, policyholders get predictability of when and how much they can get when there’s a trigger. On the insurers’ end, it promises risk predictability, since the maximum payout is fixed and known in advance, simplifying capital reserve requirements. Traditional insurance billing, however, can be unpredictable for those who prefer matching the actual financial impact of the loss.

Which Model Fits You?

The right choice depends less on which model is “better” and more on what you’re trying to protect against and how quickly you need funds after a loss.

When to Choose Traditional Insurance

Traditional insurance remains the undefeated heavyweight champion for high-severity, asset-heavy protection. If your primary goal is to ensure that a $50 million distribution center can be completely rebuilt brick-by-brick after a fire, traditional property insurance is the only mechanism equipped to handle that exact indemnification. Choose if:

Likelihood of Major Events

Assess your goal and financial model. If you operate in a high-risk environment, it is beneficial to choose traditional insurance billing. It helps to recover complete financial loss after a complex or variable loss, such as property damage, liability claims, and equipment breakdown, etc.

Pre-Existing Conditions

Traditional insurance plans provide the necessary financial safety nets when companies have pre-existing risk factors. For instance, companies carrying physical inventory, commercial autos, or liability exposure.

Business Scale and Accessibility

Healthcare providers, auto body shops, and allied fields use traditional billing to tap into large insurance provider networks, which guarantee a steady volume of patients or clients who would otherwise be unable to afford services out-of-pocket.

When to Choose Parametric Insurance Billing

Parametric insurance billing works best in scenarios where traditional insurance fails, is too expensive, or takes too long. Consider adding parametric coverages if:

You Face Uninsurable Economic Losses

Your business relies on tourism, and a nearby oil spill or algae bloom destroys your seasonal revenue, even though your physical property is untouched.

You Have Massive Deductibles

You can use a parametric policy specifically to “buy down” a massive 5% windstorm deductible on your traditional property policy, utilizing the fast parametric payout to cover your traditional out-of-pocket costs.

You Operate in High-Risk Zones

Traditional capacity for perils like wildfires or hurricanes is shrinking and becoming prohibitively expensive. Parametric structures allow you to secure guaranteed, transparently priced capital for those specific, volatile risks.

By blending the comprehensive indemnification of traditional billing with the frictionless speed of parametric triggers, modern risk managers can build a resilient, multi-layered financial defense system capable of weathering any storm.

How SubscriptionFlow Supports Both Billing Models

SubscriptionFlow automates the financial side of policy lifecycle, from premium collection to payout, across both models, offering a unified system to insurers rather than forcing them onto separate tools for each.

- For traditional billing: Automates recurring premium invoicing and payment collection, and moves claims through verification, documentation, and payment processing to cut manual admin work.

- Parametric billing: Its flexible, rules-based engine and support for multiple pricing models (flat-rate, tiered, usage-based) can be configured for pre-agreed, trigger-based payouts, though it’s not a purpose-built parametric trigger / index platform.

Choosing Your Financial Defense

In most real-world risk management strategies, the two models aren’t competitors; they’re complements. Many businesses and insurers use parametric coverage to fill specific gaps left by traditional policies, particularly where speed of payout matters more than precision, or where traditional coverage has high deductibles, exclusions, or slow claims processes for a particular peril. A common structure pairs traditional coverage as the primary loss-matching layer with a parametric policy layered on top or alongside it, providing rapid cash flow immediately after a triggering event while the traditional claim works through its standard assessment process. Ready to streamline billing across both traditional and parametric policies? Schedule a demo with SubscriptionFlow and see how automated premium-to-payout workflows can fit your business.